I hope you had a wonderful week with your spouse. Today, we’re diving into a topic that might feel a bit sensitive—money. It’s something we don’t often discuss openly, but today we’ll explore how finances can impact marriage, sometimes even to the point of causing separation.

When we take our marriage vows, we commit to being together “till death do us part.” Yet, studies show that money is the second leading cause of divorce, just after infidelity. We live in a world where infidelity is prevalent, but financial issues are a close second when it comes to breaking marriages apart. It’s surprising how something like money, which we might assume would naturally be shared between spouses, can become a divisive force.

I remember a quote from one of my former pastors: “If you’re willing to share your body with someone, why wouldn’t you share your money?” It’s a powerful thought, and it highlights how money can create problems in a marriage if not managed properly.

For instance, money can build resentment. During our premarital counseling, we were advised to have a joint account, and though it didn’t seem like a big deal at the time, it has made a significant difference over the years. Having one account or even two accounts but managing them jointly has brought us a lot of comfort. It means I can’t ask my husband to buy me something extravagant, like a Mercedes, without knowing if we can afford it. I’m aware of our family’s financial situation, and that reduces pressure.

However, I know not all couples manage their finances the same way. Some prefer to keep their money separate, where each person has their own account and pays their own bills. That’s fine if it works for them. But for us, pooling our resources has simplified our lives and prevented a lot of potential conflict.

When a couple faces financial difficulties, it’s easy to start seeing each other as the enemy. Money, after all, makes things happen. If there’s not enough to go around, blame can start to creep in. This is why I advocate for a joint account—if you can make it work. Of course, there are exceptions, especially if one spouse is financially irresponsible. But if you can agree to manage your finances together, it can make things much simpler.

Even if you don’t have a joint account, financial stress can still build resentment. You might find yourself frustrated if your spouse spends money on something you think is unnecessary, especially if you’re struggling to make ends meet. Over time, this can create a wedge between you, leading to feelings of resentment that could last for months or even years.

Financial strain also increases stress in the family. When you don’t know how you’re going to pay the bills, put food on the table, or cover your children’s school fees, it creates a lot of pressure. This stress can lead to fatigue and even depression, making it difficult to show love and affection to your spouse. Remember, love and appreciation need to be expressed, but that becomes hard when you’re overwhelmed by financial worries.

Poor communication and a lack of trust can also damage your relationship. If you’re not discussing your financial situation openly, one spouse might assume everything is fine while the other knows it’s not. This disconnect can cause serious problems.

We’ve just come through a pandemic, and many people lost jobs, businesses, and even ministries. It’s been a tough time, and if you’re not communicating well with your spouse, they might still expect you to maintain the lifestyle you had before. This can lead to more resentment and a breakdown in communication.

Financial stress can also make you see your spouse in a negative light. The very traits that attracted you to them might start to annoy you. For example, if your wife is usually joyful and laughs a lot, but you’re struggling financially, her laughter might irritate you because it feels out of place. This can turn you against each other if not addressed.

When you’re financially constrained, it also limits your opportunities as a couple. There are places you can’t go, things you can’t do, and assets you can’t acquire, which can make you feel left behind and further strain your relationship.

That’s why it’s so important to discuss money openly with your spouse, even when you’re not in a financial crisis. Sit down together and talk about your priorities, what you can afford, and what you might need to cut back on. This way, you can make decisions as a team and move forward together.

Now, let’s look at some ways to resolve financial issues in your marriage. But first, let’s turn to the Bible. Did you know that money and possessions are mentioned over 2,000 times in the Bible? That’s more than prayer! Clearly, money is an important issue to God, and He has left us with instructions on how to manage it wisely to protect our marriages.

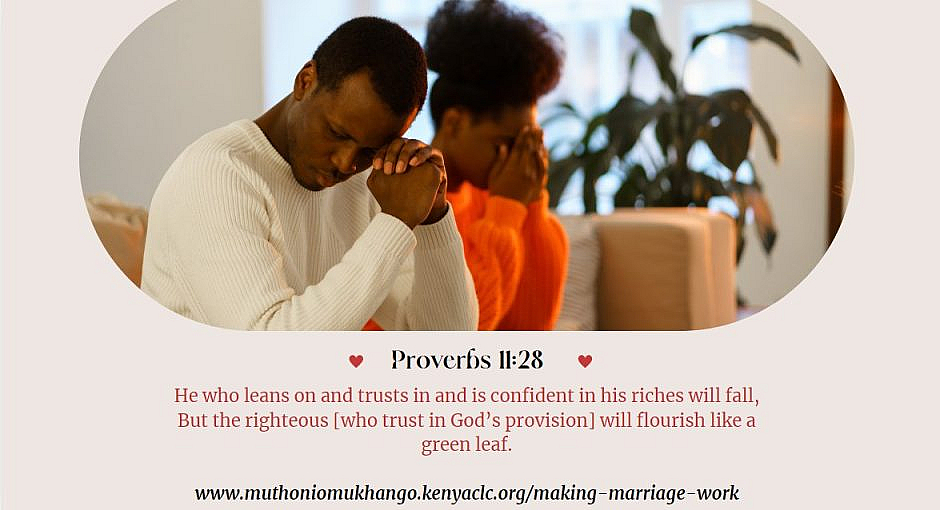

For example, Proverbs 11:28 says, “He who trusts in his riches will fall, but the righteous will flourish like a green leaf.” Money can give you a sense of confidence, but you shouldn’t place your trust in it. Your marriage should always come before money.

Ecclesiastes 5:10 reminds us that “Whoever loves money never has enough; whoever loves wealth is never satisfied with their income. This too is meaningless.” It’s great to have money, but if it becomes your main focus, you’ll never be satisfied. Instead, prioritize your spouse and your union, and the rest will follow.

Here are a few practical tips to help you manage your finances as a couple:

Talk Openly About Your Financial Problems: Share any debts or financial issues with your spouse, whether they were the result of bad decisions or good ones that didn’t work out. Your spouse needs to know where you stand financially so you can tackle the problems together.

Seek Help If Needed: If you’re really struggling, consider getting help from a financial coach or taking a financial planning class. Sometimes, a new perspective or strategy is all you need to get back on track.

Take Control of Your Finances: I recommend the book Managing Your Finances God’s Way by Gladys Juma. It offers practical advice and tools to help you take charge of your finances, get out of debt, and cultivate healthy boundaries around money.

Remember, it’s important to be content in both the good times and the bad. As Paul says in Philippians 4:12, “I know how to be brought low, and I know how to abound. In any and every circumstance, I have learned the secret of facing plenty and hunger, abundance and need.” There will be high moments and low moments in your marriage, but if you prioritize your union over money, you can weather any storm together.

May you and your spouse find contentment and peace, no matter your financial situation. God is with you in every season, and with His help, you can overcome any challenge.

𝐇𝐨𝐰 𝐝𝐨 𝐲𝐨𝐮 𝐡𝐚𝐧𝐝𝐥𝐞 𝐦𝐨𝐧𝐞𝐲 𝐢𝐧 𝐲𝐨𝐮𝐫 𝐦𝐚𝐫𝐫𝐢𝐚𝐠𝐞?

Handling money in a marriage can vary greatly depending on each couple’s preferences, values, and communication style. Here’s an exploration of the different approaches mentioned:

a. I don’t know what my spouse makes

This approach reflects a level of financial independence where each partner manages their own income and expenses separately. While it can provide a sense of autonomy, it might also lead to challenges in financial planning, transparency, and trust. In some cases, this method works well if both partners are financially secure and prefer not to mix finances. However, it might create a disconnect when it comes to shared financial goals or dealing with unexpected financial crises.

b. We know what each earns but everyone sorts assigned bills

This method combines transparency with individual responsibility. Both partners are aware of each other’s earnings, which fosters trust and openness. They split the financial responsibilities, with each person managing specific bills or expenses. This approach allows for shared financial goals while maintaining some level of independence. It works well when both partners are comfortable with their financial roles and when they have similar financial habits and priorities.

c. We have a joint account and handle all bills from there

This approach reflects full financial integration and partnership. All income is pooled into a joint account, and bills and expenses are managed collectively. This method can strengthen the sense of unity and teamwork in a marriage, as both partners are equally involved in financial decision-making. It can be particularly effective for couples with aligned financial goals and habits. However, it requires strong communication and mutual trust, as both partners need to agree on spending and saving decisions to avoid conflicts.

Each of these approaches has its pros and cons, and the best choice depends on the couple’s relationship dynamics, financial goals, and personal preferences. The key is to maintain open communication and regularly discuss finances to ensure that both partners are comfortable with the arrangement.

Here are the pros and cons of the approach where you don’t know what your spouse makes:

Pros:

Financial Independence: Each partner has full control over their own finances, allowing them to spend, save, or invest without needing to consult the other. This autonomy can be empowering for individuals who value their financial independence.

Reduced Conflict Over Money: Since finances are kept separate, there may be fewer disagreements over spending habits, savings goals, or budgeting. Each partner is responsible for their own financial decisions, which can reduce tension.

Simplified Money Management: With separate finances, each person only needs to manage their own income and expenses. This can simplify financial management, especially if one partner prefers a different style of budgeting or financial planning.

Cons:

Lack of Transparency: Not knowing each other’s income can lead to a lack of transparency, which might erode trust over time. It can also create misunderstandings or resentment if one partner feels that the financial contributions are uneven or unfair.

Challenges in Financial Planning: Without a full understanding of the household’s total income, it can be difficult to set and achieve shared financial goals, such as saving for a home, planning for retirement, or budgeting for vacations.

Potential for Financial Disparities: If one partner earns significantly more than the other, this approach can create an imbalance in the relationship. The partner with less income might feel burdened or stressed by financial responsibilities, while the higher-earning partner might feel pressured to contribute more.

Difficulty in Managing Emergencies: In the event of an unexpected financial crisis, such as job loss or a medical emergency, the lack of pooled resources could make it harder to respond effectively. It might also lead to conflicts about who should contribute more during tough times.

Disconnect in Shared Goals: Keeping finances separate can create a disconnect when it comes to long-term financial goals or large purchases. Partners might find it challenging to align their financial priorities or make joint decisions on significant investments.

This approach works best when both partners are financially stable, have similar financial philosophies, and communicate effectively about money despite their separate finances. However, it requires careful consideration and ongoing communication to ensure that both partners are comfortable with the arrangement.

Here are the pros and cons of the approach where both partners know what each earns but everyone sorts assigned bills:

Pros:

Transparency and Trust: Knowing each other’s income fosters a sense of openness and trust. Both partners are aware of the household’s financial situation, which can strengthen the relationship and reduce misunderstandings.

Shared Financial Responsibility: By assigning bills and expenses, each partner contributes to the household’s financial well-being. This approach ensures that both parties are actively involved in managing the finances, which can create a sense of partnership.

Balanced Independence: While there is transparency about income, this method still allows for individual financial autonomy. Each partner can manage their assigned expenses and have control over their remaining income, which can be important for personal financial freedom.

Flexibility in Financial Roles: This approach allows couples to divide financial responsibilities in a way that suits their strengths or preferences. For example, one partner might handle utilities and groceries, while the other manages mortgage payments and insurance.

Easier Financial Planning: Since both partners know each other’s earnings, they can more effectively plan for shared financial goals, such as saving for a vacation, paying off debt, or investing in the future.

Cons:

Potential for Imbalance: If one partner earns significantly more than the other, the distribution of financial responsibilities might feel unequal. The lower-earning partner may feel burdened or stressed if the bills they are assigned are too high relative to their income.

Risk of Financial Discrepancies: Even with transparency, there may be differences in how each partner handles their assigned bills. One partner might be more diligent about budgeting or saving, which could lead to friction if the other partner’s spending habits are different.

Less Comprehensive Financial Integration: While this method involves some level of collaboration, it doesn’t fully integrate the couple’s finances. This partial separation might make it harder to align on larger financial decisions or goals, such as buying a home or planning for retirement.

Potential for Resentment: If one partner feels they are contributing more financially or taking on more significant responsibilities, it could lead to feelings of resentment or frustration, especially if their financial contributions are not acknowledged or appreciated.

Complexity in Managing Joint Expenses: In cases where expenses fluctuate or unexpected costs arise, determining who should cover these can be challenging. Without a clear system in place, it could lead to disputes over how additional expenses should be handled.

This approach can work well when both partners have similar financial habits and a strong sense of communication. It strikes a balance between shared responsibility and individual financial autonomy, but it requires ongoing dialogue to ensure that both partners feel satisfied with the arrangement.

Here are the pros and cons of the approach where both partners have a joint account and handle all bills from there:

Pros:

Strengthened Unity and Partnership: By pooling all income into a joint account, both partners are equally involved in the financial management of the household. This approach reinforces the sense of being a team, working together towards common financial goals.

Simplified Financial Management: With all income and expenses flowing through a single account, tracking household finances becomes easier. It provides a clear overview of the financial situation, helping to streamline budgeting, bill payments, and savings efforts.

Aligned Financial Goals: Full financial integration encourages both partners to align their financial goals and priorities. This can lead to more effective planning for major life events, such as buying a home, raising children, or saving for retirement.

Enhanced Trust and Transparency: A joint account fosters transparency, as both partners have access to and visibility over all transactions. This openness can build trust, as there are no financial secrets between partners.

Shared Responsibility: Handling all bills and expenses together ensures that both partners are equally responsible for the household’s financial well-being. This can reduce the burden on one partner and promote a fair distribution of financial duties.

Cons:

Potential for Conflicts: Managing a joint account requires strong communication and mutual agreement on spending and saving decisions. Disagreements over financial priorities or spending habits can lead to conflicts if not managed carefully.

Loss of Financial Independence: Some individuals may feel a loss of autonomy when all finances are combined. Without a personal account, partners might feel restricted in their ability to spend money freely or pursue individual financial goals.

Vulnerability in Case of Relationship Strain: If the relationship encounters difficulties, having fully integrated finances can complicate matters. Separating finances during a breakup or divorce can be more challenging, and one partner might feel vulnerable if they rely heavily on the joint account.

Risk of Overspending: With both partners accessing the same account, there’s a risk that one might overspend, leading to insufficient funds for essential bills or savings. This requires careful coordination and communication to avoid financial strain.

Unequal Contributions: If one partner earns significantly more than the other, the higher-earning partner might feel that their contributions are not proportionate to their spending power. Conversely, the lower-earning partner might feel pressure to contribute more than they can comfortably afford.

This approach can be very effective for couples who are closely aligned in their financial habits, values, and goals. However, it requires ongoing communication, trust, and a shared vision for how finances should be managed to ensure that both partners feel satisfied and secure in the arrangement.

Mismanagement of money in marriage brings resentment! What measures have you put in place to safeguard your marriage?

ismanagement of money in marriage can be a significant source of resentment, leading to stress, mistrust, and even marital breakdown. When financial responsibilities are not handled well, one partner may feel burdened, unsupported, or unfairly treated, which can erode the foundation of love and respect in the relationship.

To safeguard your marriage from the pitfalls of financial mismanagement, consider implementing the following measures:

Open Communication: Regularly discuss your financial situation with your spouse. Be transparent about your income, debts, and spending habits. Open dialogue helps to align your financial goals and ensures that both partners are on the same page.

Joint Financial Planning: Create a budget together that reflects your shared priorities and goals. Whether it’s saving for a home, planning for children’s education, or setting aside money for retirement, working together on a financial plan strengthens your partnership.

Joint or Separate Accounts: Decide on a banking system that works best for both of you. Some couples find joint accounts helpful for managing household expenses, while others prefer separate accounts with shared responsibility for bills. The key is to agree on what works for your relationship and ensure transparency regardless of the approach.

Prioritize Expenses: Establish what’s most important to your family’s well-being and focus your spending on those priorities. This could include housing, food, education, and savings. By prioritizing, you reduce the likelihood of unnecessary expenditures causing friction.

Seek Financial Education: Consider attending financial management classes or reading books on personal finance together. Educating yourselves on financial matters can empower you to make informed decisions and avoid common pitfalls.

Plan for Emergencies: Set up an emergency fund to cover unexpected expenses. Having a financial cushion can reduce stress during tough times and prevent financial difficulties from escalating into bigger issues.

Regular Financial Check-ins: Schedule regular check-ins to review your financial situation. This allows you to make adjustments as needed and ensures that both partners remain involved in the financial management of the household.

Respect Differences: Recognize that each partner may have different attitudes toward money. Some may be spenders, while others are savers. Understanding and respecting these differences can help you find a balance that works for both of you.

Debt Management: If you have debts, work together to create a plan for paying them off. Avoid blaming or shaming each other for past financial mistakes. Instead, focus on how you can move forward together.

Professional Help: If financial issues become overwhelming, consider seeking help from a financial advisor or counselor. A professional can offer objective advice and help you create a plan to improve your financial situation.

By taking these proactive steps, you can protect your marriage from the strains that money mismanagement can bring, fostering a relationship built on trust, mutual respect, and shared goals.

Subscribe to join me, let's journey together...

2 comments On Till Money Do You Two Apart? The Date is 2016 (Fifth Year in Marriage)

Pingback: The Order of Priority in Marriage: How to Build Intimacy in Marriage. The Date is 2017 (Sixth Year in Marriage) - Reflections By Muthoni Omukhango ()

Pingback: Marriage-Remarriage - Reflections By Muthoni Omukhango ()